KeywordsERM Governance Practices Intellectual Capital Organizational Performance

JEL Classification G32, L25, L30, O34

Full Article

1. Introduction

Successful economic performance and value creation are considered as the major drivers for an enterprise in a dynamic business environment. Enterprise risk management has been highly considered by today’s corporate managers as a strategic approach to managing risks faced by business entities in a holistic way as oppose to traditional silo-based risk management. Despite there being growing concerns on the adoption of ERM practices with the key objective of enhancing firm value, there is little empirical evidence supporting the value relevance of the ERM implementation. Prior researchers have made some attempts to empirically verify the relationship between ERM and firm performance and mixed results have been observed on the value relevance of the ERM implementation.

A comprehensive program for managing business risks provides an important foundation for sustaining competitive advantage (Economist Intelligence Unit, 2007). Therefore, ERM frameworks adopted by organizations are based on practical issues and technical methodologies within the business environment. In view of risk governance practices, one of the core mandates of boards is risk oversight. Good boards hold all their members responsible for risk oversight. They interact directly with management on risk matters; ensure the ERM organizational model is optimized for each risk by reporting, evaluating and deciding the appropriate risk response. COSO, (2004) refers ERM as a top-down approach. Therefore, it is pre-requisite for board members and senior management to buy-in risk governance practices for meaningful ERM implementation and success. The author further states that, without support from the top-level, efforts made to identify, measure and control risks will fail to link up with business decision making, resulting to minimal impact on strategic planning and organizational performance. Consequently, risk governance practices ensure that an organization has developed procedures and internal controls which are essential in order to avoid loss, maintain security and enhance profitability. It also includes an infrastructure that enables everybody to improve transparency and know their responsibility (Lai, Azizan and Samad, 2010). In other words, it supports internal flow of information which is necessary for making relevant and timely decisions. Further, it allows the organization to flourish and survive in the market.

On the other hand, Hussinki et. al, (2016) states that intellectual capital (IC) focuses on all the intangible assets that an entity may consume to realize competitive advantage. Furthermore, IC includes three perspectives: human capital which discusses an entity’s employees and their insights, abilities, education, aptitudes and attributes; besides, structural/organizational capital denotes that IC is possessed and rests with the entity even when individuals go home; and finally, relational/social capital is the worth entrenched in and gotten from relationships with clients, service providers, partners, organizations, and other equivalent stakeholders. According to Khan and Ali, (2017) valuable intellectual assets in an organization may resolve issues relating to risk management in respect to risk policy, oversight of internal controls, accountability, board strategy and monitoring of management functions.

Performance of SCs has been worrying over a period with the global reporting of high profile corporate failure (Enron, Worldcom), Global Financial Crisis (2008) and the reporting of corporate scandals within organizations Kenya. Consolidated financial statements for all State Corporations (SCs) for the period ending 30th June 2016 prepared by National Treasury indicate that there was a decline in surplus by fifty-nine per cent (59%) from an aggregate of Kshs 246 million reported in 2014/15 to Kshs 100 million in 2015/2016. An annex to the consolidated financial statement shows that forty-three per cent (43%) of the all the SCs reported losses in 2015/16FY. The poor performance has even extended to some major state corporations engaged in profit making activities. For instance, in the Ministry of Agriculture, all the four sugar companies reported significant losses including Muhoroni Sugar Company Ltd which has been placed under receivership for poor performance reported a deficit of Kshs 257 million.

Performance of SCs has a critical role in enabling the government achieve her constitutional obligation of bringing about social economic development in the country through provision of efficient services to the citizens (CGD, 2010). There have been great discussions on the causes of variations in performance of organizations. Ombaka et al.,(2015) posit that explaining why firms in the same industry and markets differ in their performance remains a fundamental question within management circles. ERM has partly been used to explain performance differences among organizations. Further, organization with higher intellectual capital are more likely to endure effects of unforeseen changes within the market. Studies by (Kamukama, Ahiauzi and Ntayi, 2011) show that organizations have assets which boosts their competitive advantage and performance. Porter (1999) opines that the crucial requirement for an organization’s success in a competitive environment is to employ resources that are unique and specific to the firm. Consequently,organizations with high levels of intellectual capital are probably going to withstand the impacts of unexpected changes in business sectors. In addition, (Sofian et al.,2014) opines that such organizations can effectively anticipate their risk exposure and handle them in a better way. Therefore, this study explored the relationship between ERM and organizational performance when moderated by intellectual capital. As a result, the study hypothesized that:

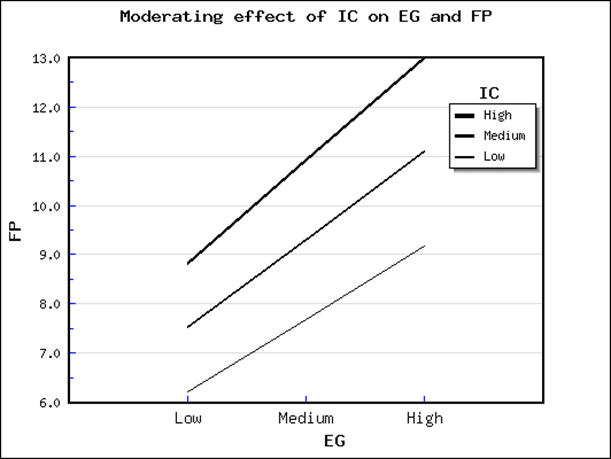

H: The effect of risk governance practices on organizational performance is moderated by intellectual capital.

2. Literature Review

2.1 Theoretical Review

Resource-based theory proposes that resources owned by the firm positively influence its performance (Barney, 2002). Resource-based theory (RBT) considers internal resources and capabilities that an organization owns and evaluates the value potential of those resources in creating its worth. This aids the organization in defining its strategy so as to attain value maximization in a sustainable way. Therefore, RBT supposes that resources and capabilities are fundamental for superior performance. It assumes that there is a heterogeneity of resource endowments between organizations and explains the (sustained) competitive advantage of an organization through the possession of resources with certain characteristics. An organization should possess resources that are valuable (V), rare (R), inimitable (I) and non-substitutable (N) so as to achieve a sustainable competitive advantage. Grant (1991) opines that resources can be tangible or intangible assets that are important inputs in production and delivery of products and services. This study sought to apply the VRIN criteria as the basic pillars of holistic ERM. This is because ERM seeks to manage all risks in harmony within a coordinated and strategic framework rather than to manage risks independently (Nocco and Stulz, 2006).

Studies by Bromiley and Rau (2016) indicate that resources cannot be productive by themselves. Therefore, managers should be able to deploy those resources in an effective and efficient manner. Further, an organization’s strategy should be synchronized to its environment of business operation. As defined by COSO (2004), ERM is part of an organization’s strategy for enhancing performance. Thus, for an entity to achieve competitive advantage over others, its managers need to identify ERM practices that are critical for the firm and explore them into full capacity. RBT uses a strategic choice such as ERM to enable the organization identify, develop and deploy key resources so as to maximize its returns (Fahy, 2000). Hence, organizations invest in processes and routines underlying their dynamic capabilities so as to manage risks. The resource-based view provides a framework that helps to set priorities in risk management. Due to environmental complexities, organizations are subjected to an unlimited amount of potential risks (Bromiley and Rau, 2016, Burisch and Wohlgemuth, 2016). Management may not handle all of them once and needs to identify and focus on potential threats with the greatest impact on the firm. Applying the resource-based view clarifies which risks the firm should focus on.

2.2 Previous Studies

Erin, Asiriuwa, Olojede and Usman (2018) investigated the influence of risk governance on performance of money deposit banks in Nigeria. Panel data was collected from a sample of eleven listed Nigeria banks for the period of 2012 to 2016. Bank performance was measured using ROA while risk governance was measured by use of proxy variables such as presence of Chief Risk Officer (CRO), Centrality of CRO, independence of the Board Risk Committee, Activism of Board Risk Committee, Board’s independence and ERM score. Secondary data the study variables were collected from annual reports of the selected banks. The study controlled for firm size, audit committee independence, board size, cost to income ratio and loan. The study used descriptive statistics, correlation and fixed effect regression model to analyze the data. The study found that all the risk governance variables except Centrality of CRO had a positive and significant impact on the performance of listed banks in Nigeria. The results of this study are consistent with those of (Nahar et al., 2016; Mollah et al., 2014).

Cavezzali and Garddenal (2015) examined the influence of risk governance on firm performance as evidenced by Italian listed banks. The study obtained data from twenty-one banks listed at Borsa Italiana for the period starting from 2005 to 2013.Secondary data was obtained from published reports on; financials, corporate governance and remuneration from the company websites and Borsa Italiana webpage. Firm performance was measured using both ROE and ROA while risk governance was measured by proxy using CRO presence, board of directors’ independence, risk committee activism, CRO centrality and experience by risk committee. The study controlled for bank profitability, bank size, operating efficiency (cost to income ratio.) and capital structure. The data was analyzed using fixed effects regression model. The study obtained mixed results on the influence of risk governance on firm performance. CRO presence and CRO centrality were not statistically significant while Risk Committee experienceand its activism level had a negative effect on ROE and ROA. Further, board independence was not significant. However, experience by risk committee representing their professional background could help lower the overall level of risk.

Aebi, Sabato, and Schmid, (2012) did an enquiry on whether risk management-related corporate governance instruments; for example, attendance of CRO in policymaking board of a bank; and whether the CRO is accountable to the Chief Executive or straight to the board of directors, were connected with a superior bank performance for the period of 2007/2008 financial crisis. Bank performance was estimated by use of buy-and-hold returns and ROE. The study did control for the usual corporate governance factors like CEO ownership, board size, and board independence. Data was collected the year 2006 and time series regression used to analyze the data. The results indicated in banks which the CROs accounts for their activities directly to the board of directors and not to the Chief Executive (or other corporate organs) stock returns and ROE were considerably higher (i.e., less negative) stock returns during financial crisis. Unexpectedly, most standard corporate governance factors were irrelevant or even adversely related to the banks’ performance during the crisis.

Similarly, Battaglia and Gallo (2015), studied the effect of risk governance on Asian bank performance during financial crisis. The paper investigated whether boards of directors and risk management mechanisms related to corporate governance are associated with better bank performance during the financial crisis of 2007/2008. The study focused on banks listed in China and India. Bank performance was measured using Tobin's Q, ROA, return on equity (ROE) and price–earnings ratio (P/E). The study had mixed results on the relationship between risk governance and bank performance. Banks with larger risk committee had better performance in terms of profitability (ROE and ROA) for the period 2007–2011. Contrary, market valuation and expected market growth rate (Tobin's Q and P/E) was greater for banks with risk committees which were smaller. This suggests that market valuation is adversely affected by risk committee size and significantly affected by the number of risk committee meetings. This indicates that the market, discounts as auspicious the information related to “strong” risk governance.

Ponnu (2008), examined the effect of corporate governance structures, particularly board structure and CEO duality, on the performance of Malaysian public listed companies. Data was collected from 100 Bursa Malaysia companies for the period 1999 to 2005. Firm performance as measured by return on assets and return on equity. Mann Whitney U Test was used to analyze the data. The study found that that there is no significant relationship between corporate governance structures and company performance.

Studies that have be carried out on ERM and organizational performance have focused on different study variables such as determinants of ERM adoption, characteristics of firms that adopt ERM, in addition to identifying ERM practices within an organization. Further, disentangling the influence of intellectual capital on organizational performance is of importance to SCs because they rely on intangible resources and capabilities to a great extent. Further, according to Togok and Suria, (2014), most studies done on the effect of ERM on performance or value creation are based on experiences from developed countries like USA, United Kingdom, Germany, Canada representing 75%. On the contrary, Asian and Middle East countries represent 18% and 5% respectively, while other developing countries represent 2% of the studies. Moreover, companies in high regulated nature of industries; insurance and financial services were always chosen in most ERM related studies. However, research posit that despite ERM being a concept that is accepted worldwide, it is always implemented and interpreted in local ways (Tekathen and Dechow, 2013). There is a gap believed to be in the wider social, institutional and organizational context in which ERM operates, rather than just focusing on the technical aspects of risk management (Soin and Collier, 2013). That is, examining the operations of ERM within the actual organization settings. The context of SCs in Kenya in this study is an area of interest because they were established to provide essential services as well as improve service delivery to the public and enhance efficiency. Therefore, their performance is of keen interest to government, general public and other stakeholders. In addition, Bhimani, (2009) posits that risk management is ultimately a social construct shaped by the contexts they inhabit. Consequently, this study sought to join this debate by investigating the moderating role of intellectual capital on the influence of ERM governance practices on organizational performance.

3. Research Methodology

3.1 Research Design and Target PopulationThe study used explanatory cross sectional survey design. A survey was carried out on 218 state corporations in Kenya in the year 2019. Primary data on ERM governance practices, intellectual capital and organizational performance was collected from structured questionnaires. The questionnaire was designed on a five point Likert -type scale ranging from (1) - strongly disagree to (5) – strongly agree. The target respondents were Finance Managers in SCs because they are best placed to answer the research questions. Collier et al. (2007) asserts that finance managers play a critical role in risk management.

3.2 Measurement of Variables

The study has operationalization and measured of the study variables as indicated in the Table 1.

Table 1. Operationalization and measurements of variables

| Variables | Operational Indicators | Measure | Supporting Literature |

| Organizational Performance | Composite index of organizational performance (Financials, customers perspective, internal business process, learning and growth) | 5- point likert scale type questions | Calandro and Lane (2006) Marques and Simon (2006) |

| ERM Governance Practices | integrated ERM strategy, accountability, compliance and risk reduction | 5- point likert scale type questions | Lai and Shad (2015) Bozkus (2014) |

| Intellectual Capital | Human capital, structural capital, relational capital | 5- point likert scale type questions | Cabrita and Bontis (2008) Bontis et al., (2000) |

| Firm Size | Measured as natural logarithm of total assets | Ordinal scale | Beasley et al., (2005) Hoyt and Leibenberg, (2008) |

| Growth rate | Percentage increase in revenue of the organization | Ratio scale | Beasley et al. (2005) |

| Industry differences | 1=financial sector, 2= commercial and manufacturing, 3= public universities, 4=training and research,5= service corporations, 6=tertiary education and training, 7=regional development, and 8=regulatory sector | Nominal scale | Waweru and Kisaka, (2013) |

| Level of ERM implementation | 1=Not at all, 2=Plans to introduce, 3= Adhoc implementation, 4=Implemented but needs improvement, 5=Robustly implemented | Nominal scale | Beasley et al. (2005) Waweru and Kisaka, (2011) |

Source: Researcher (2019)

3.3 Model specification

To test the moderation effect of intellectual capital on the relationship between ERM governance practices and organizational performance, the study used hierarchical regression model (baron and Kenny, 1986). Further, the study controlled for growth rate, industry differences and firm size. The effect on the dependent variable (organizational performance) was regressed on controls, exogenous variables and interactions terms. The hierarchical regression models were done by entering variables in lump of variables for control and exogenous variables including the moderator as well as each of the interaction terms and observing their results as outlined below in the equations:

Y = β0 + β1C1+ β2C2+ β3C3+ ξ1 (1)

Y = β0 + β1C1+ β2C2+ β3C3+β4X1 + ξ1 (2)

Y = β0 + β1C1+ β2C2+ β3C3+β4X1+ + β5M+ ξ1 (3)

Y = β0 + β1C1+ β2C2+ β3C3+β4X1+ β5M+ β6M.X1+ ξ1 (4)

where

Ci : Represents Firm Characteristics (Control variables); where C1 (Firm size), C2 (Growth rate) and C3 (Industry differences).

Xi : Represents ERM Governance Practices (independent variables)

Mi : Represent Intellectual Capital (moderator variable)

Yi : Represent Organizational Performance (dependent variable)

4. Results and Discussions

4.1 Response Profile

The study intended to collect data from 218 respondents. However, data was successfully collected from 197 respondents. This represents a response rate of 90.4 percent of the target population, which falls within the confines of a large sample size (n ≥30). This provides a smaller margin of error and good precision (Draugalis et al., 2008). Further, to examine the level of ERM implementations in State Corporations, frequency tables and percentages were used as indicated in Table 2. The results indicate that 43.7% of the state corporations have implemented ERM but the need improvement and 18.8% have had ad hoc implementation. Only 15.7% of the state corporations have robustly implemented ERM. On the negative side, 4.6% of the not implemented ERM while 17.3% have plans to introduce it.

Table 2. Level of ERM implementation

| Frequency | Percent | ||

| Implemented ERM | Not at all | 9 | 4.6 |

| Plan to Introduce ERM | 34 | 17.3 | |

| Ad hoc Implementation | 37 | 18.8 | |

| Implemented but Improvements needed | 86 | 43.7 | |

| Robustly implemented | 31 | 15.7 | |

| Total | 197 | 100 |