Keywordsdebt demographics education financial illiteracy informal saving interest rates and inflation Midrand recession retirement Savings spending behaviour

JEL Classification D14, P46

Full Article

1. Introduction

Saving is crucial in accumulating assets, promoting financial well-being and creating a channel out of poverty. Saving also leads to financial freedom. Individuals with savings are able to absorb negative economic changes (Lewis and Messy, 2012, p.7). On a macro-economic level, lack of saving hinders the economic growth of the country. There is too much saving in informal saving platforms, which may lead to inadequate financial instruments. Recession has contributed to an increase in unemployment and increased poverty, which has affected savings and investment. Chiroro (2010, p.3) highlighted that saving and investment options have become more complicated and individuals need to acquire financial knowledge. In South Africa, excessive spending and lack of financial planning are amongst the key factors that affect savings behaviour.

The South African economy is picking up, but the majority of South Africans are struggling to save. The savings behaviour in Midrand is of great concern. Households are reluctant to save, even though they are aware of the benefits. High levels of unemployment, financial illiteracy and being in debt negatively affect savings. This research seeks to unravel factors which influence savings in Midrand.

The objectives of this study are:

• To investigate the saving methods used by people.

• To determine the benefits of saving.

• To examine the factors hindering saving.

• To make recommendations that would improve the saving behaviour.

The study aims to improve the living conditions of the community as it will help people who are struggling to save. It is anticipated that the research can be used to assist government and households in finding ways to increase savings, which is critical in igniting investment. The paper offers a summary of traditional theories relevant to the research, as well as some background to the savings behaviour of households.

2. Literature Review

A synopsis of traditional theories explains the savings behaviour of households and discusses the sources of funding for South African citizens.

2.1. What are Savings?

Saving for an unforeseen situation or saving for retirement has not been easy for South Africans. Savings and investments need to be differentiated. Savings is money kept in a safe platform, and allows access to the funds, but with less returns. Investment is a riskier option, but returns may be higher. Higher savings in a country bring healthy investments. This gives rise to industrial growth (Rehman et al., 2011, p.269; Zwane et al., 2016, p.209). Household saving has two components: discretionary and contractual saving:

· Discretionary saving is a saving platform where there is no fixed contract.

· Contractual savings refers to a contractual obligation to make payments.

Hoos (2010, p.18) states that saving has influenced the number of dependents, lifespan of the individuals, level of income and education, and that because households are demographically different, they will not have similar saving behaviour. There are various types of saving, discussed below.

2.1.1. Personal Saving

Household saving is money kept in a bank account, in personal saving. Patel (2017) offered tips to help Midrand residents cut out unnecessary expenses and avoid wasting money, including paid for television and store-bought water, in this regard.

2.1.2. Saving for Retirement

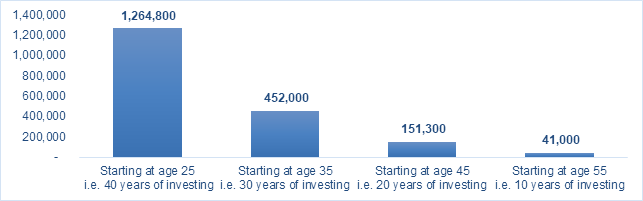

Saving for retirement is for the needs one may have in post-working life. Vistawealth (2016, p.29) states that in order to achieve retirement goals, one should start saving early as it allows one to profit on compound interest. Figure 1 depicts these advantages.

Figure 1. Advantage of starting to save early (currency R)

Source: Adapted from Stanlib (2014, p.05)

The South African population is characterised as a consumption-led and excessive borrowing economy. Chauke (2011, p.19) states that even though income measures for the middle-class are improving, there is still a culture of borrowing rather than saving.

2.1.3. Saving by General Government

Saving by general government is the sum of the retained earnings of public businesses and retained taxes. It is different to households whose income contains factor earnings. Table 1 shows the savings by general government.

Table 1. Saving by General Government

| R millions | 2014 | 2015 | 2016 | |||||||

| 4 | 2014 | 1 | 2 | 3 | 4 | 2015 | 1 | 2 | 3 | |

| Taxes on production and imports (6004K) | 130223 | 478479 | 137103 | 114031 | 130137 | 138821 | 520092 | 154897 | 120994 | 141590 |

| Current Taxes on income and wealth (6251K) | 149960 | 558057 | 163225 | 148698 | 138495 | 156163 | 606581 | 176994 | 159757 | 150392 |

| Net saving (6202K) | -762 | -85001 | 10656 | -19364 | -40066 | -5610 | -54384 | 15505 | -15867 | -43753 |

| Seasonally adjusted annualized rates | ||||||||||

| Taxes on production and imports (6004L) | 501425 | 478479 | 510318 | 522820 | 513597 | 533633 | 520092 | 574179 | 554353 | 559396 |

| Current Taxes on income and wealth (6251L) | 570540 | 558057 | 594662 | 669073 | 568189 | 594400 | 606581 | 644529 | 717888 | 617379 |

| Net saving (6202L) | -63826 | -85001 | -65946 | -9345 | -52995 | -89250 | -54384 | -69291 | -3299 | -52748 |

Source: South African Reserve Bank

2.1.4. National Saving

With reference to Figure 4, Rehman et al. (2011, p.268) see national savings as an important element in attaining high economic growth. To understand South African savings and its factors, the apartheid legacy must be taken into account. Black Africans were negatively affected by apartheid, and their ability to save was greatly affected (Zwane et al., 2016, p. 210- 211). Savings related to government, and private savings are linked to the private sector. The private sector can be regarded as the country’s commercial sector and households (Zwane et al., 2016). There has been extensive experimental literature investing the factors of household savings in South Africa (Chipote and Tsegaye, 2014, p.184). This has mainly focused at macro-economic variables.

Table 2. National income and saving

| R millions | 2014 | 2015 | 2016 | |||||||

| 4 | 2014 | 1 | 2 | 3 | 4 | 2015 | 1 | 2 | 3 | |

| Gross national income at market prices (6016K) | 953732 | 3711063 | 950326 | 978472 | 974656 | 1009772 | 3913226 | 1003703 | 1041235 | 1045455 |

| Real gross national income (at 2010 prices) (6016C) | 758793 | 2933767 | 738732 | 757109 | 739370 | 765140 | 3000351 | 719748 | 752133 | 747046 |

| Gross saving (6203K) | 162044 | 589390 | 156005 | 187978 | 156933 | 156831 | 657747 | 127413 | 202126 | 179876 |

| Seasonally adjusted annualized rates | ||||||||||

| Gross national income at market prices (6016L) | 3786171 | 3711063 | 3820126 | 3908019 | 3919939 | 4004820 | 3913226 | 4073684 | 4151547 | 4205723 |

| Real gross national income (at 2010 prices) (6016D) | 2948709 | 2933767 | 3017840 | 3011898 | 2980924 | 2990742 | 3000351 | 2958389 | 2990321 | 3009793 |

| Gross saving (6203L) | 648938 | 589390 | 687038 | 677564 | 632545 | 633847 | 657747 | 627348 | 717736 | 712420 |

Source: South Africa Reserve Bank - Quarterly Bulletin (2016)

2.1.5. Advantages and Disadvantages of Saving

The savings system educates people on the discipline of saving and using money wisely. There is no enforced discipline when personal saving is banked. Most households believe that saving money in a bank is a waste of time, as they think the banks use that money for their gain.

2.2. Traditional Theories of Household Saving

Traditional theories are used to explain how individuals save. The significance of Keynesian`s theory will be discussed here, as well as permanent income, and the life-cycle theoretical hypotheses.

2.2.1. Keynesian Interpretation of Savings Behaviour

Keynesian theory formed part of a major foundation of studies conducted on savings behaviour of households. Keynes`s theory supported the idea that savings was considered a luxury. Keynes (1936) was one of the first researchers to recognise saving goals, as listed below:

· For unexpected situations

· For forthcoming needs

· To earn interest and grow capital

· To improve and better one’s standard of living

· To self-finance and gain a sense of being independent

· To invest money into an organisation

· To leave money to beneficiaries

· To satisfy greed

These savings goals support the fact that people across different stages of life save for different reasons. Saving is equal to investment, according to Keynes (1936). This notion contradicts the state of South African consumers, who have a consumption and debt culture (Cronje and Roux, 2010, p.27).

2.2.2. Permanent-Income Hypothesis

Friedman (1957) puts forward the permanent-income hypothesis (PIH), which distinguishes between transitory and permanent elements of income as aspects of household savings. He argues that wealth is made up of human and non-human wealth. Permanent income is seen as the inflow of income resulting from the use of assets, skills and talent. To have an understanding of household saving behaviour, the focus should be on the size of the household income and the expenditure.

2.2.3. Life-Cycle Hypothesis

This hypothesis assumes that households plan their lifetime consumption and do not leave behind any assets for their beneficiaries (Fisher, 1907; Modigliani and Brumberg, 1954). Life-cycle hypothesis (LCH) focuses on the savings behaviour of households (Nga, 2007, p.11). It examines the gathering of assets during earning years and maintaining the consumption standard during retirement. The core purpose of saving with regard to LCH is for retirement and to gain wealth. A person can prolong their lifetime earnings by accumulating savings during their working periods and use it when they retire (Adewuyi et al., 2010, p.83), who emphasise that individuals of working-age are able to accumulate more assets. The last phase is when the individual reaches post-working age and has no income (Abu et al., 2013, p.57). In the South African context, Mongale et al. (2013, p.520) highlight the relationship between income and saving, by using the Integrating Vector Autoregressive framework (CVAR). Household savings is influenced by the increase in income.

2.3. Sources of Funding and Saving

2.3.1. Income

Income can dictate people’s spending and saving habits - when they earn more, they tend to spend more and save some. Those earning less tend to spend less and save none. Personal income is the income from wages, salaries etc. (Laudon and Bitta, 2006, p.51).

2.3.2. Unemployment and Low-Income Levels

The inability to earn an income makes it impossible to start saving. About 35.5 million people i.e.70% of South Africans (Chiroro, 2010, p.2), earn less than R12 200 per annum. One of the significant requirements for economic growth of the country is financial marketing that will enable people to save. The significant aspects of saving are as follows (Gurusamy, 2011, p. 2):

· Mobilising of saving – This refers to obtaining money from savers such as household individuals, businesses, public sector and others.

· Investment - Banks play a key role in collection of the funds from clients.

· National Growth - Banks help the growth of the country’s economy by ensuring a flow of surplus money to deficit areas.

· Entrepreneurship Growth - Financial institutions help entrepreneurs by making financial resources available.

· Industrial Development - The different components of financial markets help to boost the growth of industry.

2.3.3. Education

An educated individual understands the benefits of savings (Laudon and Bitta, 2006, p.51). Saving behaviour can teach people how to differentiate between needs and wants.

2.3.4. Occupation

There are differences in families when it comes to saving. It differs by how much they work and the money they get paid. Households, smaller in size, tend to manage their expenditures better and are able to save. However, there are households that are unable to save due to their low income.

2.3.5. Poverty, Inequality, and Development

In developing nations, poverty is the reason why households cannot save and it is a widespread challenge, according to Todaro and Smith (2009, p.143), who note further that over 40% of the global population lives on less than R16 a day. Factors that affect poverty, inequality and development are:

· Income inequality - This defines the income distribution and poverty problems that characterise many developing nations (Schwab, 2014, p.59).

· Size Distributions – Todaro and Smith (2009, p.209) suggest that most economists use the size distribution of an income.

· Measuring Absolute Poverty – This is the magnitude of absolute poverty in developing nations.

2.3.6. The Relatively Rich Save More

Rich people tend to save more. Although real income has increased, the saving rate has not. In South Africa, Thakersee (2005) reports that rich people are saving less. This is supported by Nga (2007, p.5), who states that rich and educated individuals lack a saving culture, but their spending habits have increased.

2.3.7. Saving Goals and Saving Behaviour

Bucks and Pence (2006) mention the characteristics of savers and non-savers, and that the reasons why people save has not received much attention compared to why people do not save.

2.4. Why are South African Households Not Saving?

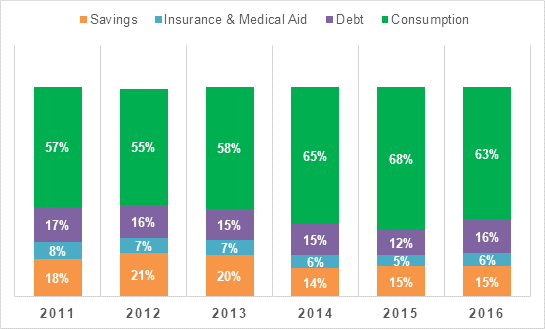

Low-income and middle-income groups in South African find it difficult to save for emergencies or for their retirement. About 72% of South African adults do not save, while 80% have not changed their savings (Erasmus, 2015). South Africans are characterised as being in debt, according to Cronje and Roux (2010, p.27). They state that a low saving level may be the result of a debt-ridden economy. Figure 2 illustrates the spending behaviour of households.

2.5. Interest Rates and Rate of Inflation

Interest rates play an important role in investment and savings: the higher the interest, the higher the return (Nga, 2007, p.18). The cost of borrowing is higher when the interest rate is high. Nga (2007, p.18) states that “the impact of interest rates on saving is uncertain”. The rise in inflation rates may lead to higher nominal rates, and as a result, households save more.

Figure 2. Saving as a percentage of household income

Source: Old Mutual Savings and Investment Monitor (2016, p.15)

2.6. Financial Literacy

Financial literacy may be defined as having the necessary skills and knowledge in order to make sound financial decisions (Lewis and Messy, 2012). Lack of financial literacy means people cannot budget or plan their financial goals, especially in South Africa, where the quality of education and illiteracy is high. The Census (2011) reported that Midrand “education levels in the region are good with about 57 747 people with grade 12 or higher education”. Hence the residents’ financial literacy ought to be adequate.

Savings are thus defined differently by different stakeholders within the country. This paper provides the theory related to saving and investment, and a clear view on why people do not save enough. Also highlighted, is that people save for different reasons.

3. Research Methodology

Polit and Hungler (2004, p.233) describe research methodology as the technique of obtaining, arranging and analysing data. Research design technology is used to get information for making business decisions and is the way to systematically solve the research problem.

3.1. Sampling and Data Collection

When using a sample, it is important to differentiate between the target population and the sampled population (Trochim, 2006, p.38). Blumberg et al. (2008, p.228) describe target population as the total group of people from which a researcher needs to make readings (Blumberg et al., 2008, p.228). The target population in this study was the households in the Midrand area.

The quantitative research method aims to analyse the predictors of a certain total population; therefore, the sample size is of paramount importance (Stokes, 2013, p.48). The aim of sampling is to assess unknown characteristics of the whole population. (Stokes, 2013, p.47) states that the sample size should to be sufficiently predicated in order to make statistically precise interpretations.

In the Midrand sample population, the researchers took into consideration demographics of the households such as gender, race groups and age. The researcher used the sample size calculator equation to determine the sample size from the target population. From the population of the Midrand, the sample size was for households was 188. For this study, a questionnaire was the chosen instrument for data collection. Kothari (2003, p.124) argues that a questionnaire is viewed as the main tool to conduct the study and if not constructed well, then the chances of it failing are high. The questionnaire was managed through the use of Monkey Survey and sent to participants via email. It highlighted factors that contribute to their savings behaviour and mentioned measures that can help them and improve their saving behaviour.

The questionnaire was constructed in a closed-ended questions format, including single choice and rating levels using the 5-point Likert-scale rating. The components below were considered in the questionnaire:

· Age - Is the age of individuals a factor in saving behaviour?

· Education - Is there a link between the level of education and saving behaviour?

· Culture - Do parents educate children about the importance of saving?

· Level of income – Does the household level of saving increase as income increases?

3.2. Pilot Study

A pilot study was conducted amongst 10 respondents, in which valuable understanding was gathered, and necessary amendments to the questionnaire were made.

3.3. Data Analysis

Burns and Grove (2003), as cited in Mamabolo (2009, p.63), describe data analysis as a process of collecting data, the interpreting and converting it to draw conclusions that can be used to make decisions and changes.

In order to analyse the saving behaviour of the households, the questionnaire was categorised into the following segments:

· Demographics - comprising gender and age;

· Psychological elements – this included short-term consumption versus long-term benefit;

· Education elements – this included financial literacy.

The data analysis conducted is generally descriptive and inferential, as the purpose of the study was not to compare households but to investigate their savings behaviour. The Kruskal-Wallis test was used to determine the relationship between two variables.

3.4. Validity and Reliability

In order to guarantee that the research quantifies what it supposed to quantify, the research must have a validity component (Saunders et al., 2012, p.276). The pilot study tried to ensure that the validity was taken into consideration. The questionnaire was also administered to two senior employees at the work place, who were not part of the research study. These individuals critically analysed the validity of the questionnaire.

The researcher used information obtained in the literature review to construct questions. The questions were administered online. A reliability test was piloted, whereby five questions were asked to examine whether the households understood the basic financial aspects, such as interest rate and budgeting.

3.5. Limitations of the Study

· The study covers only Midrand suburbs.

· Quantitative research allows the researcher to have a vigorous analysis. It does not offer an explorative analysis, so it does not provide opportunity for new findings.

· It is difficult to validate that all the participants are Midrand residents.

· It is assumed that respondents to the survey represented their households, so their savings behaviour is aligned to the spouse.

· Some participants may hesitate in providing personal information about their earnings.

3.6. Elimination of Bias

Bias is regarded is one of the main weakness of questionnaire or self-report. Otto (2009, p.102) states that only individuals who have sufficient knowledge regarding the topic should participate in the questionnaire It was highlighted to the participants that the questionnaire was confidential and there were no right or wrong answers. The researcher was aware that money is a sensitive issue, so the study was introduced as money management instead of saving behaviour.

3.7. Ethical Considerations

Polit and Beck (2004, p.717) as cited in Maboe (2006, p.69) describe research ethics as a method of moral values, which is to make sure that the researcher adheres to the legal, professional and social rules to study participants. In order to ensure elimination of bias, the selection of participants, data collection and sampling was random.

In this research study, the researcher complied with the following ethical guidelines as described by Trochim (2006):

· The researcher made it clear that the survey was a voluntary participation and that no individual was obliged to respond. The participants were informed that information provided was only for research purposes.

· The researcher ensured the confidentiality and anonymity of the participants (Sekaran and Bougie, 2013, p.44).

· The researcher ensured that no harm would come from participation in the research study. Participants have a right to be protected (Cooper and Scheidler, 2014, p.31).

4. Results, Discussion and Interpretation of Findings

A total number of 191 responses were received over 36 days. The questionnaires were sent via email to 369 participants (a response rate of 51.76%) and the researcher took to social media by posting the web link questionnaire. The responses were considered as acceptable feedback.

Due to the different format used in the construction of the questionnaire, the Cronbach’s Alpha approach was used to determine the reliability of the items.

4.1. Demographics

This addresses elements such as gender ratio, age, salary level, race and educational level.

The gender ratio was spread fairly across the genders of the participants; females at 55.5 % and males 44.5%. 55.5% of responses were received from participants between the age of 22 and 35, followed by 34% from participants aged between 36 and 45, then 7.3% from participants between the ages of 46 years and above. Those aged 21 and below constituted 3.1% of the respondents.

47.4% respondents were single and married respondents constituted 47.9%. Divorced respondents constituted 4.2% and the widowed less than 1%. 78.3% of the responses were from blacks; 10.1% were Indian and 7.4% white. Coloureds constituted 4.2%.

The majority of respondents were employed full-time at 83.7% and 11.1% were self-employed. The remaining percentage of 6.3% was shared by 2.1% of people who were not employed and 3.2% were employed part-time. 44.5% of the respondents were holders of a degree or honours degree, followed by 29.3% with diploma qualifications. 6.3% of the respondents had a matric or lower as their highest qualification. Masters and PhD qualifications made up 5.2%

40% of household monthly salaries were on the upper level of the scale, followed by 14.7% of salaries between R 25 000.00 to R30 000.00. Only 4.7% of the households were on monthly salaries of between R0 and R 5 000.00. 61.1 % of the respondents had an additional source of income, while 38.9 % did not.

Some 39.8% of the respondents had studied banking, investment and insurance, followed by 17.8% who studied accountancy and 13.6% who studied engineering.13.6%. studied media and marketing 7.9% and 3.7% respectively. 2.1% studied medicine; the rest of the study fields shared 15.1%

4.2. Section B: Descriptive statistics analysis and interpretation of research questions

This section offers the analysis and interpretation of the research questions aligned to the study objectives.

4.2.1. Research question 1: Which methods of savings do people prefer, and to what length did they save?

· Retirement annuity

60% of the respondents have a retirement annuity as opposed to 40%, who did not. Abu et al. (2013) affirm that middle-age is usually the age to pay off some debts as retirement is imminent. The majority of the households have retirement annuity, which is positive.

· What is the proportion of monthly saving/investment to your household income?

The majority of households saved between 3% and 10% of their income, followed by 25.5 % of those who saved less than 2%. It is clear that households do not save enough. According to the South Africa Institute of Savings, a person or household should save at least 20% of their net income.

· Are you a member of group saving scheme/“Stokvel”?

Participants were asked if they were part of any group saving schemes such as “Stokvels”. 65% did not belong to any group saving platform, while 35% did.

· How are savings invested?

Participants were asked which methods of savings they preferred. 31% put their savings in a normal savings accounts; 23% in 32-day notice accounts; 16% and 12 % preferred unit trusts or exchange-traded fund and property respectively, and 12% preferred shares. The remaining 5% preferred gold, policies, bitcoin and just less than 1% chose nothing.

4.2.2. Summary

The findings show that the majority of households have retirement annuities to secure financial well-being post-working years. The participants also preferred to save through group schemes. There is a concern that the majority of the households have lower yield savings accounts. A lack of financial knowledge of other investment products may be the cause.

4.3. Research question 2: Are households educated enough to understand the benefits of saving?

Questionnaire analysis and interpretation

Below is an analysis of the 10 questions relating to research question 2. Each question was analysed taking into account the answers received from the participants.

· Budget Skills

Just over 55% of the respondents were confident with their budget skills; 24% were not so confident, and 21% were either confident or not. Only 22% of the respondents were strongly confident about their budget skills. The results indicate that most of the respondents reported being confident with their budget skills. As 94% of the population holds a post-matric qualification, this brings into question the curriculum and quality of the education in South Africa. Laudon and Bitta (2006, p.51) state that education brings about understanding of future saving.

· Payments on financial commitments

Over 87% of the participants knew how much they paid on their house, car and other financial commitments, 10% either knew or did not know. Less than 3 % of the participants did not know. The majority of the households knew the interest rate they paid on credit commitments.

· Do you have insurances to cover for unexpected events; such as life cover, funeral cover, car and home insurance?

85% of the respondents did have insurance to cover for unexpected events and 15 % did not.

· I am in debt

Over 46% of the respondents were in debt; 11% of those were highly in debt; 35 % of the respondents were not in debt and 19% were not sure. This is not surprising as the country is characterised by a “buy now and pay later” attitude (Cronje and Roux, 2010, p.27).

· I do understand the importance of saving

The majority of the respondents (93%) did understand the importance of saving; 5% either understand and only 2% did not understand.

· I think I will retire comfortably

Some 46% of the respondents indicated that they will retire comfortably, 32% were not sure and 22% acknowledged that they would not.

The majority of the research population was between 22 and 35 years of age, and that is when one should be thinking about retirement. In order to achieve retirement goals, one should start saving early (Vistawealth, 2016, p.29). This was supported by the Life-cycle hypothesis theory. The elderly often do not save in order to meet their day-to-day needs.

· I do educate my children about the importance of saving

The majority of participants did educate their children about the importance of saving. Only 9% did not talk about money matters with their children.

· Do you think your current investment could bring return above inflation?

Some 39% of the participants believed that their savings and investments would bring return above inflation; 33 % were not sure and 28% disagreed.

· Do you think government and the private sectors are doing enough to educate the population about the importance of savings?

Only 13% of the participants agreed that the government and private companies were doing enough. 16% neither agreed nor disagreed and 71%, which was the majority of the participants, disagreed. Most respondents did not think that there were financial literacy initiatives by the government and private companies.

4.3.1. Summary

Although these households have higher levels of education, they still lack financial literacy. Households did understand the benefits and importance of saving, although some did not understand the financial concepts. It is important to mention that few participants, who understand the financial markets and management of their personal finances, said it was a great concern that the majority of households lacked basic financial literacy skills. Overall, households were educated, but they fell short on important aspects of personal finances and they did not save enough.

4.4. Research Question 3: What contributes to the savings behaviour among households of the Midrand area?

· I know how much I spend every month

Some 68% of the respondents knew how much they spent every month; 20% neither agreed nor disagreed and only 12% did know their monthly expenditure. This result suggests that 32% of the households did not know. One would not expect such a large number from an educated population not to know their monthly expenses. Individuals spent a major part of their income on day-to-day expenses and are left with little or no money for saving (Kotzè and Smit, 2008, p.157).

· I stick to my budget and reconcile every month

The majority of the respondents did not stick to their budget. Some 31% disagreed and 12% strongly disagreed. 23% of the respondents were not sticking to a budget and 35% of the participants agreed. Without a proper budget in place, one cannot plan purchases (Chauke, 2011, p.82).

· I know how much I spend on entertainment monthly

Some 52% of the respondents did know their monthly expenditure on entertainment, 24% were unsure and 24% did not know. Individuals without proper financial education spend a large portion of their income on entertainment (Chauke, 2011, p.82).

· I do comparison of prices before purchase

71% of the participants compared prices before they bought an item, while 14% were unsure, and 15% did not.

4.4.1. Summary

There are a large number of households that did not know their monthly expenditure. Many households did not stick to their budget and the majority of participants did not know their monthly entertainment expenditure. Over 70% of the households indicated that they compare prices before shopping.

Instant gratification and lack of financial literacy are the main contributors in the poor saving behaviour. That the majority of the households did not know their monthly expenditure, is disturbing.

4.5. Further findings: Purpose of saving

Over 40% of the households save for unforeseen expenses; 20% to settle debts, followed by 11% for a deposit for a house, and 7% to buy a new car. According to Old Mutual (2016), South Africans save in the following order: 43% save for rainy days, 37% for retirement and funeral costs, 22% save for education for their children, 18% to settle debts, 16 % for improving their home and 13% save for deposit for a vehicle and maintenance.

· If I were to resign from my current employment, I would cash my pension fund

43% acknowledged that they would not cash in their pension fund when they resign; 39% would, and 18% were undecided.

· Does level of income influences savings?

There is an increase saving with the growth of income. Households with higher income save relatively more. A closer analysis of the Kruskal–Wallis result between the variables indicated that the more the income, the higher the saving. The outcomes are in-line with the research study by (Zwane et al., 2016, p.210).

5. Conclusions and Recommendations

While there was no evidence suggesting that certain racial groups save more than others, blacks with lower-and-middle income are the biggest participants (45%) in group savings e.g. “Stokvels”. The National Stokvel Association of South Africa (NASASA) estimates that there are more than 800 000 “stokvels”, with an estimated economy of R49b. Very few of the “stokvels” are for investment and wealth creation purposes.

Financial literacy plays a major role in selecting a savings vehicle; being knowledgeable makes it the easier to make well-informed choices. Over 50% of the participants save their money in a 32-day notice account, and other typical saving accounts, with low interest and low risk.

The majority of South Africans struggle against poverty and low-income levels, which hamper disposable income. Many South Africans find it difficult to put money aside in case of emergencies and even for their retirement. About 72% of adults do not save, while 80% have not increased their savings. About 35.5 million (70% of South Africans) earn less than R12 200 per annum (Chiroro, 2010, p.4). Only one third between ages of 18 and 30 are putting money away for retirement.

Bucks and Pence (2006) highlight that the borrowers do not seem to understand the impact in changes of interest rates on their income and adjust their spending and saving accordingly.

The following are the shortcomings of South Africans due to lack of financial literacy:

· More than half of the population considers death, funeral and disability covers to be more important than saving for retirement (Old Mutual, 2016, p.18).

· It is important for parents to teach saving behaviour to their children at early age (Chauke, 2011, p.26).

· They lack understanding of inflation and its impact. In order for the investor to create wealth on investment, the money invested should bring a return above inflation.

The government and private entities have a responsibility to educate the public about saving and investment. It is in the best interests of both for the country to have a healthy saving culture.

Regarding what contributes to the savings behaviour, the following findings emerged:

· A barrier to saving is high unemployment and low-income levels.

· Budgeting is one of the most important aspects of planning personal finances.

· Financial illiteracy may result in inefficient decisions (Nga, 2007, p.20).

· Financial literacy structured programmes in education would help literacy.

· According to LCH, households build assets during their working years in order to retire comfortably (Abu etal., 2013, p.57). South Africans are an excessive expenditure and credit driven population. This indicates that most citizens would not retire comfortably.

· Lack of retirement savings contributes excessively to government expenditure.

· It has been reported that the rich save more. Post-1994, households regarded as middle-class, do not save enough.

· Chauke (2011, p.27) characterised the black middle-class as people who tend to buy expensive clothes, cars and houses in order to compete.

· Instant gratification is a major stumbling block for the savings culture.

Households do not save enough and most prefer low-risk saving accounts. Even though 60% had retirement annuity in place, 40% of the respondents did not. Post-working age they will rely on family members and the government to manage. Most respondents indicated they save between 3% and 10% of their monthly income, but this is not enough for future goals.

The findings indicate that the households do not save as much as they should. The majority save between 3% and 10% of the monthly income, which is below the 20% mark recommended by the Institute of Savings. The second objective of the research study concerned the benefits of saving. It can be concluded that the benefits of saving are to secure a financial well-being, which also contributes positively to the growth of Midrand and the entire country. The third objective concerned the factors hindering saving. There were a number of factors identified which influenced such behaviour.

5.1. Recommendations

Good savings behaviour is important for any country and for the financial independence of its citizens. It is critical for the government and private sector to find ways to improve the saving culture.

The following are recommendations to stimulate the savings culture of households in Midrand:

· Financial education in primary and secondary schools.

· There should be compulsory sessions for employees to be educated about the importance of saving.

· Withdrawal of 100% pension and provident funds should be prohibited, or limited.

· Parents should encourage their children to start saving.

· Tax incentives – products such as tax-free savings account should be widely communicated.

Although the above recommendations may improve the savings culture of Midrand households, more practical measures should be investigated before implementation.

The aim of the research study was to investigate the savings behaviour of the households in Midrand. The findings indicate that households in Midrand do not save enough and lack financial education. The findings of this research study are in line with the literature review, which indicates the advantages and disadvantages of saving. It has been proven that if one does not save, it disadvantages financial independence and future prospects.

References

- Abu, N. Zaini, M. Karim, A. and Aziz, M., 2013. Low savings rate in the Economic Community of West African States (ECOWAS): The role of political instability-income integration. South East European Journal of Economics and Business, 8(2), pp. 53-63.

- Adewuyi, A. Bankole, A. B. and Arawomo, D. F., 2010. What determines saving in the Economic Community of West African State (ECOWAS). Journal of Monetary Economic Integration, 10(2), pp. 71-96.

- Amaratunga, D., Baldry, D., Sarshar, M., and Newton, R., 2010. Quantitative and Qualitative Research in the Built Environment: Application of “mixed” Research Approach. Work-study, 51 (1): pp.17-31.

- Blumberg, B., Cooper, D.R., and Schrindler, P.S., 2008. Business Research Methods. 2nd ed. Berkshire: McGraw-Hill Education.

- Bucks, B., and Pence, K., 2006. Do homeowners know their house values and mortgage terms?. Federal Reserve Board of Governors, Federal Reserve of the United States of America, 1-38.

- Census, 2011. Main Place Midrand. [online] Available at: http://census2011.adrianfrith.com/place/798004: [Accessed on 26 May 2017].

- Chauke, H.M., 2011. The determinants of household saving: The South African Black middle-class perspective. Gordon Institute of Business Science: University of Pretoria., Mini-dissertation- MBA).

- Chipote, P. and Tsegaye, A., 2014. Determinants of Household Savings in South Africa: An Econometric Approach (1990-2011). Mediterranean Journal of Social Science, 5(15).

- Chiroro, B., 2010. Savings should drive economic recovery and economic growth in South Africa. http://www.savingsinstitute.co.za/campaign_archives/festive10/SW%20Report.pdf [Accessed 13 February 2017].

- Coleman, S.T., 2013. Permanent Income. [online] Available at: http://closemountain.com/wp-content/uploads/2017/03/PermanentIncome_1.pdf [Accessed on 22 April 2017].

- Cooper, D. and Schindler, P., 201. Business Research Methods. 12tg Edition. New York: McGraw Hill Education.

- Cronje, M. and Roux, A., 2010. Creating a savings culture for the black middle class in South Africa-policy guidelines and lessons from China and India. USB LEADERS’ LAB, Volume 4 no. 2, 2010, University of Stellenbosch.

- Du Plessis, G., 2008. An exploration of the determinates of South African’s personal savings rate - Why do South African households save so little?. Gordon Institute of Business Science: University of Pretoria, Mini- dissertation- MBA.

- Erasmus, S. 2015. South Africans among the world’s worst savers. Fin24: 01, 07 July. [online] Available at: http://www.fin24.com/Savings/News/South-Africans-among-the-worlds-worst-savers-20150707 [Accessed on 22 June 2017].

- Friedman, M., 1957. A Theory of the Consumption Function. Princeton: Princeton University Press.

- Geek, W., 2010. What is data analysis? [online] Available at: ww.wisegeek.com/whatis-data-analysis.htm [Accessed on 10 April 2017].

- Gurusamy, S., 2009. Capital Market. 2nd ed. New-Delhi: McGraw Hill.

- Hair, J, F., Money, A.H., Samuel, P., and Page, M., 2010. Research Methods for Business. 2nd ed. USA: John Wiley and Sons.

- Hoos, K., 2010. Saving Behaviour in Cebu City. Master’s Thesis. Utrecht University.

- Keynes, J. M. 1936. The general theory of employment interest and money. London: Macmillan.

- Kothari, C. R., 2003. Research Methodology. 5th ed. New Delhi: McGraw-Hill.

- Kotzè, L and Smit, A.V.A., 2008. Personal finances: What is the possible impact on entrepreneurial activity in South Africa. Southern African Business Review, 12(3), p.159.

- Lewis, S. and F. Messy., 2012. “Financial Education, Savings and Investments: An Overview”, OECD Working Papers on Finance, Insurance and Private Pensions, No. 22, OECD Publishing. http://dx.doi.org/10.1787/5k94gxrw760v-en. Accessed 29 April 2017.

- Laudon D.L, and Bitta, D. A. J., 2006. Consumer Behaviour Concepts and Applications. 4th ed., New Delhi: McGraw-Hill.

- Maboe, K.A., 2006. Computer Assisted Instruction in Nursing Education. Pretoria: University of South Africa., Dissertation – MBA.

- Mahlo, N., 2011. The determinants of household savings in South Africa. University of Johannesburg. Thesis.

- Mäkelä, P., Mustonen, H., and Österberg E., 2007. Does beverage type matter? Nordic Studies on Alcohol and Drugs. 24(6), pp.617–631.

- Mamabolo, L.R.C., 2009. The experiences of registered nurses involved in the termination of pregnancy at Shoshanguve community health centre. Health Studies: University of South Africa., Dissertation - MBA.

- Mashigo, P. and Schoeman, C., 2010. Stokvels as an instrument and channel to extend credit to poor households in South Africa: An inquiry. Policy Paper 19. University of Johannesburg.

- Mongale, I.P. Mukuddem-Petersen, J. Petersen, M. A. and Meniago, C., 2013. Household saving in South Africa: An Econometric Analysis. Mediterranean Journal of Social Sciences, 4(13), pp. 519-530.

- Modigliani, F. and Bumberg, A., 1954. Test of the life cycle hypothesis of saving. Bulletin of the Oxford Institute of Statistics, 19, pp. 99-124.

- Modigliani, F., 1986. Life-Cycle, Individual Thrift, and the Wealth of Nations. American Economic Review, 76, pp.297-313.

- Naidu, P., 2017. Employee Perceptions of Quality at a selected company. Durban: University of Technology., Dissertation- MBA).

- Nga, M., 2007. An investigative analysis into saving behaviour of poor households in developing countries, with specific reference to South Africa. Research report for the degree of Masters in Economics, University of Western Cape.

- Ogbokor, C. A., 2014. A time series analysis of the determinants of savings in Namibia. Journal of Economic and Sustainable Development, 5 (8), pp. 52-63.

- Old Mutual Saving and Investment Monitor, 2016. Old Mutual Saving and Investment Monitor. [online] Available at: https://www.oldmutual.co.za/docs/default-source/default-document-library/omsim-2016-july_lynette-n.pdf?sfvrsn [Accessed on 28 April 2017].

- Otto, A.M.C., 2009. The Economic Psychology of Adolescent Saving. UK: University of Exeter (Thesis - PhD).

- Patel, N., 2017. Tips on how to stop wasting money this year. Midrand Reporter: January 2017. http://midrandreporter.co.za/145630/tips-on-how-to-stop-wasting-money-this-year: Accessed 29 April 2017.

- Peter, K.A., 2010. The Interpretation and use of Mixed Methods Research Within Programme Evaluation Practice. Cape Town: University of Stellenbosch., Dissertation-MBA.

- Polit, D. and Hungler, B., 2004. Nursing Research, Principles and Methods. Philadephia, Lippincourt.

- Polonsky, M. J. and Waller, D. S., 2005. Designing and managing a research project: A business student's guide. Thousand Oaks, CA: Sage Publications.

- Prinsloo, J., 2000. The saving behaviour of the South African economy. South African Reserve Bank Occasional Paper, 14, pp.1-34.

- Rehman, H. Bashir, F. and Faridi, M. Z., 2011. Saving behaviour among different income groups in Pakistan: A micro study. International Journal of Humanities and Social Science, 1 (10), pp. 268-276.

- Saunders, M., Lewis, P., and Thornhill, A., 2003. Research Methods for Business Student. 3rd ed. England: Pearson.

- Saunders M., Philip L., and Thornhill A., 2007. Research Methods for Business Students. 4th ed. England: Pearson.

- Saunders, M., Lewis, P., and Thornhill, A., 2009. Research Methods for Business Student. 5th ed. England: Pearson

- Saunders, M., Lewis, P., and Thornhill, A., 2012. Research Methods for Business Students. 6th ed. England: Pearson.

- Schwab, K., 2014. The Global Competitiveness Report 2014–2015: Annual Competitiveness Report. [online] Available at: www3.weforum.org/docs/WEF_GlobalCompetitivenessReport_2014-15.pdf [Accessed on 23 April 2017].

- Sekaran, U. and Bougie, R., 2013. Research Methods for Business. 6th ed. United Kingdom: John Wiley and Sons Ltd.

- Simleit, C. Keeton, G. and Botha, F., 2011. The determinants of household saving in South Africa. Studies in Economics and Econometrics, 35 (3), pp. 1-20.

- South Africa Reserve Bank., 2016. Quarterly Bulletin, December 2016. [online] Available at: https://www.resbank.co.za/Lists/News%20and%20Publications/Attachments/7588/12Statistical%20tables%20%E2%80%93%20National%20accounts.pdf [Accessed on 23 April 2017].

- South African Savings Institute, 2014. An Overview of Savings in South Africa. http://www.savingsinstitute.co.za/ [Accessed on21 April 2014].

- Stanlib., 2014. Principles of investing for retirement. [online] Available at: http://www.stanlib.com/Documents/Brochures/Retirement/Principles_Investing_Retirement.pdf [Accessed on 29 April 2017].

- Statistics Canada, 2010. Survey Methods and Practices. Canada: Catalogue 12-587-X.

- Stokes, R., 2013. eMarketing: The essential guide to marketing in a digital world. 5th ed. Cape Town: Quirk Education.

- Streubert-Speziale, H.J. and Carpenter, D.R., 2003. Qualitative Research in Nursing: Advancing the Humanistic Imperative. 3rd ed. Philadelphia: Lippincott Williams and Wilkins.

- Swanson, R.A., 2005. The Challenge of Research in Organizations. In R.A. Swanson and E. F. Holton (Eds.), Research in organizations: Foundations and methods of inquiry (pp. 3-26). San Francisco: Berret-Koehler.

- Tavakol, M. and Dennick, R., 2011. Making sense of Cronbach’s alpha. International Journal of Medical Education, 2, pp.54-55.

- Terre Blanche, M., Durrheim, K., and Painter, D., 2006. Research in practice: Applied methods for the social sciences. 2nd ed. Cape Town: University of Cape Town Press.

- Thakersee, A., 2005. Rich people not saving. Fin24, 10 October 2005. [online] Available at: http://www.fin24.com/Economy/Rich-people-not-saving-20051026?pageNo=1 [Accessed on 28 April 2017].

- Todaro, M.P and Smith, S.C., 2009. Economic Development.10th ed. Harlow, England: Addison-Wisely.

- Trochim, W. M., 2006. The Research Methods Knowledge Base. 2nd edition. [online] Available at: http://www.socialresearchmethods.net/kb [Accessed on 25 May, 2017].

- Vistawealth., 2014. Retire like a boss - A how to guide. [online] Available at: http://vistawealth.co.za/wp-content/uploads/2016/11/Finweek_Full_Retirement_ENG.pdf [Accessed on 29 April 2017].

- Wagner, C., Kawulich, B. and Garner, M., 2012. Doing Social Research: A global context. New York: McGraw Hill Education.

- Wakabayashi, M. and Mackellar, L., 1999. Demographic trends and household savings in China. Interim Report, International Institute for Applied System Analysis.

- Welman, J.C., Kruger, S.J., and Mitchell, B., 2005. Research Methodology. 3rd ed. Cape Town: Oxford University Press Southern Africa.

- Wilson A., 2003. Marketing Research: An Integrated Approach. 7th ed. London: Prentice Hall.

- Zwane, T. Geryling, L. and Maleka, M., 2016. The determinants of household savings in South Africa: A panel data approach. International Business and Economics Research Journal, 15(4), p.10.

Article Rights and License

© 2019 The Authors. Published by Sprint Investify. ISSN 2359-7712. This article is licensed under a Creative Commons Attribution 4.0 International License.